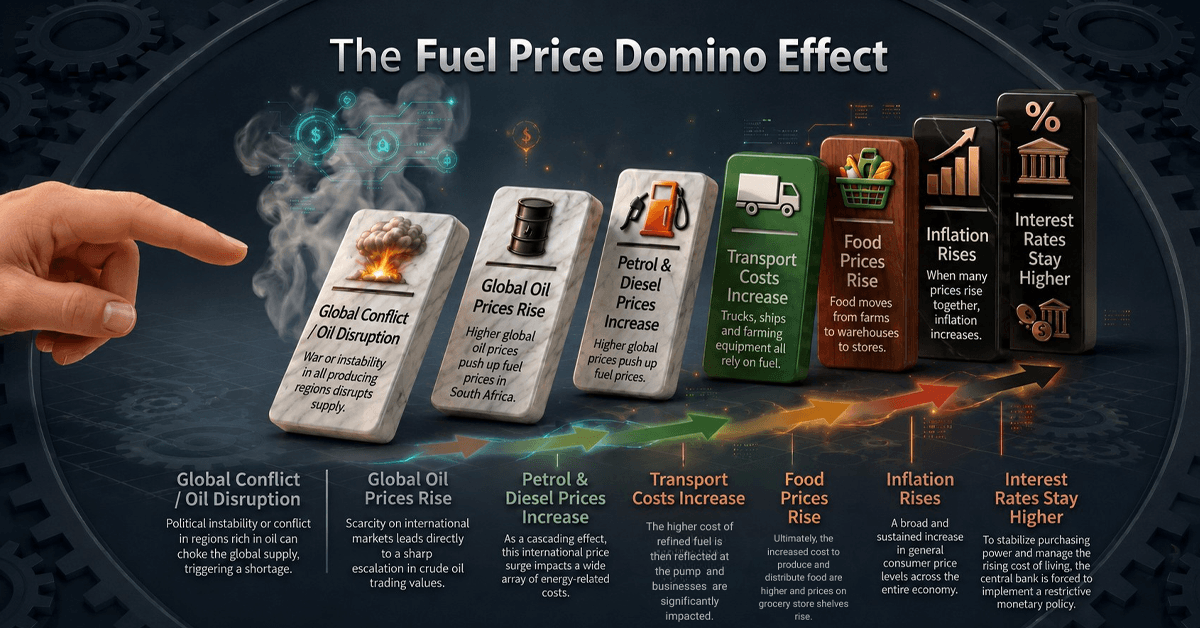

Things are about to get much harder for a lot of us. It’s a lot to take in. Between the Eskom hikes at the beginning of April and the fuel price climbing despite the R3 reprieve, 'tightening the belt' doesn't even begin to cover it, while the conflict in the Middle East has pushed oil prices up, driving fuel prices even harder.

The economic climate is set for a perfect storm, so much so that even the government couldn’t stop the record-breaking increase and decided to introduce a R3 temporary reprieve to the fuel levy. While this reprieve protects us all against the initial shock, the reality remains that we are paying significantly more to get less.

When fuel costs rise, transport costs rise too, and with that the price of food and other daily necessities. Consumers are already under a lot of strain, and this is set to add even more pressure to very tight household budgets.

The sad part for consumers is that one price increase hardly ever stays on its own. Higher fuel costs make it more expensive to move goods across the country. That pushes up food prices in stores. Higher electricity costs mean businesses spend more to keep running, and many of those extra costs get passed on to customers. Put simply, people pay more monthly to have less than they had a year ago.

At the same time, people have less money left after paying for the basics like food, fuel, and electricity and this has its own ripple effect when consumers start to cut back on basics. Businesses have fewer sales, smaller purchases, and slower payments. This usually hits small-business owners, freelancers, and anyone who depends on steady customer spending. The reality is straightforward; income drops as costs keep rising.

Debt is often where the pressure hits hardest. Monthly repayments stay the same, or even go up as interest rates rise, but the consumer does not get a salary increase. The debt repayments start to feel much heavier and harder to keep up with. Some consumers start to miss payments or fall behind. Others do their best to keep up by relying more on credit just to get through the month. Credit can bring short-term relief, but it does not last. At some point, credit limits get reached, and the room to juggle starts to disappear.

Many times there will be early warning signs when money issues begin to spiral out of control. Typically these signs include difficulty paying for the normal day to day necessities like fuel, utilities, groceries as well as having to utilize credit to meet everyday expenses. Other common signs of financial strain include delayed bill payments and excessive anxiety related to each upcoming bill due date.

Many individuals tend to continue to "keep the lights on" until their financial struggles become overwhelming. Therefore, taking immediate action typically provides an individual with more resources and flexibility to address their financial difficulties, but taking action too late creates significant obstacles in addressing your financial challenges.

An important first step in managing your finances is to assess your situation with a professional who has experience working within the area of debt. The goal of meeting with a debt counsellor is to provide clarity and practicality regarding assessing your current income and debt obligations. While the objective of the assessment is not necessarily to make a hasty decision, but rather to understand which alternatives may be available to you. Options such as lowering monthly payments, extending the length of your repayment schedule or restructuring your debt into a manageable format that fits your lifestyle are examples of ways a debt counsellor can assist you in regaining control over your finances.

Many individuals have reported feeling a great sense of relief after receiving guidance from a debt counsellor. They report that assistance provided them with the ability to create additional breathing room in their monthly budgets and reduced stress associated with making timely payments. They also report that they were able to develop a clear understanding of their future financial direction.

While South Africa may not be experiencing the same type of economic growth as other countries, costs throughout the country are increasing for reasons that are outside of an individual's control, including inflationary pressures worldwide. The most critical factor is how consumers manage the increased pressure and what actions they take to protect their personal financial interests.

Things are getting harder, not easier. Ignoring the problem will not make it disappear. Speak to a debt counsellor for practical advice and see what options are open to you in the difficult months ahead.